Why More Americans Are Exploring Roth Strategies for Retirement

Welcome To The Real Roth Strategy

This is for savers and Federal Employees with $250K+ in Retirement Accounts. A personalized Roth strategy that may help you shift from tax uncertainty to a more predictable, tax-efficient retirement plan.

The Real Roth Strategy, created by 1 Oak Financial

Ready to Get Started?

Our short survey helps determine if this strategy matches your needs—and whether you may move forward with 1.oak Financial.

Takes less than a minute. No obligation.

WHAT IS THE THE REAL ROTH STRATEGY

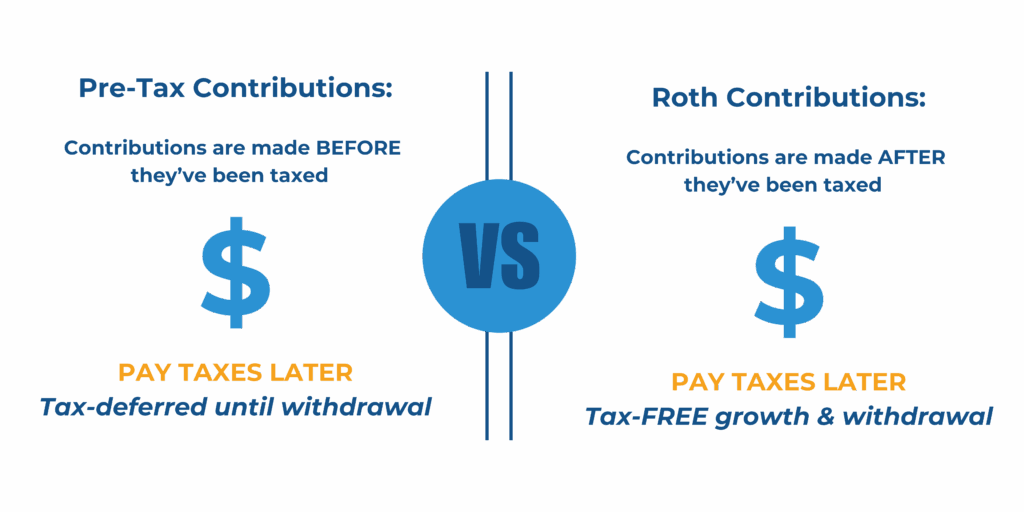

The Real Roth Strategy is a smart, tax-efficient method for moving money from a traditional retirement account (like a 401(k) or traditional IRA) into a Roth account — giving you more control over your future income and taxes.

HOW IT WORKS

You convert some or all of your existing retirement savings from a pre-tax account into a Roth account.

When you convert, you pay ordinary income tax on the amount converted now. But once it’s in the Roth account, your money grows tax-free — and qualified withdrawals in retirement are tax-free.

Because Roth accounts do not force required minimum distributions (RMDs) during your lifetime, you retain flexibility: you can draw from them when you want — or let them grow — without being forced to take distributions just to meet RMD rules.

It’s designed for savers who value long-term planning and risk management, and who want a clearer understanding of how their money may be positioned based on their individual goals and risk tolerance.

Why This Strategy Works

Tax-Free Growth & Withdrawals — Once in the Roth account, money grows without tax, and withdrawals in retirement are tax-free.

Avoid RMDs During Lifetime — Since Roths aren’t subject to required minimum distributions, you can control when (or if) you withdraw your money.

Flexibility & Predictability — Paying taxes now (at a presumably known rate) offers certainty rather than guessing about tax rates in the future.

Legacy & Estate Planning Benefits — If you don’t need to use the funds, Roth accounts can allow you to leave more to heirs without burdening them with tax on withdrawals.

Strategic for High-Savings or Higher-Income Individuals — Especially beneficial for those with $250K+ (or more) in retirement savings — giving them a tax-efficient way to convert and diversify rather than relying solely on tax-deferred accounts or pensions.

It’s a solution for savers who want predictable growth, long-term stability, and a clear plan for their money—without taking on unnecessary risk.

What You Should Know

This isn’t a do-it-yourself account. A 1.oak Financial Specialist will set it up and walk you through the details to ensure it fits your goals.